CIBIL Score and its impact on home loan

Did you have problem in getting home loan approved? Chances are your CIBIL score is not well maintained.

The CIBIL TransUnion Score is a 3 digit numeric summary of your credit history which indicates your financial & credit health. The higher your score, the higher are the chances of your loan application getting approved! The score plays a critical role in the loan approval process. It’s a record of your credit history. i.e past loans or credit cards availed from various loan providers who are members of CIBIL.

How does CIBIL get hold of your personal financial details:

CIBIL Mechanism – This is how CIBIL functions

CIBIL collect and maintain records of individuals’ and non-individuals’ (commercial entities) payments pertaining to loans and credit cards. These records are submitted to them by banks and other lenders on a monthly basis; using this information a Credit Information Report (CIR) and Credit Score is developed, enabling lenders to evaluate and approve loan applications. A Credit Bureau is licensed by the RBI and governed by the Credit Information Companies (Regulation) Act of 2005.

Why is it important to a home buyer?

First thing first, CIBIL score plays a major role in deciding the home loan limit. You avail maximum home loan, you CIBIL Score should be over and above 750.

The CIBIL TransUnion Score plays a critical role in the loan application process. After an applicant fills out the application form and hands it over to the lender, the lender first checks the credit score and credit report of the applicant. If the credit score is low, the lender may not even consider the application further and reject it at that point. If the credit score is high, the lender will look into the application and consider other details to determine if the applicant is credit-worthy. The credit score works as a first impression for the lender, the higher the score, the better are your chances of the loan being reviewed and approved. The decision to lend is solely dependent on the lender and CIBIL does not in any manner decide if the loan should be sanctioned or not.

About 80 per cent of all approved retail loans for individuals are based on the credit score given by CIBIL, which is seen as sign of creditworthiness of a loan applicant, based on his financial track record for the previous 36 months.

CIBIL has access to data on 400 million bank customers, which it uses to generate scores ranging from 300 to 900. Loans are generally sanctioned for applicants with scores greater than 750.

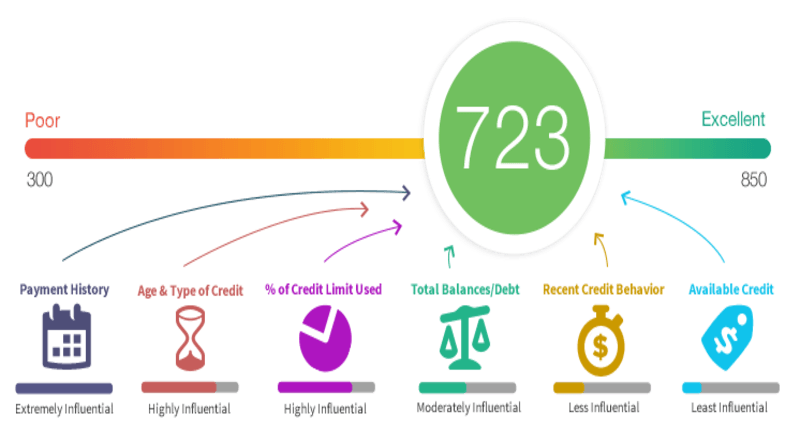

What affects my CIBIL Score?

There are 4 major factors that affect your score

Payment history: Making late payments or defaulting your EMIs or dues (recently or consistently) shows you are having trouble to pay your existing credit obligations and will negatively affect your score.

High utilization of Credit Limit: While increased spending on your credit card will not necessarily affect your score in a negative manner, an increase in the current balance of your credit card indicates an increased repayment burden and may negatively affect your score.

Higher percentage of credit cards or personal loans (also known as unsecured loan): Having a balanced mix between the secured loans (such as Auto, Home loan) and unsecured loan (such as Personal loan, Credit Card) is likely to have a more positive affect on your score.

Many new accounts opened recently: If you have recently been sanctioned multiple loans and credit cards, then lenders will view your application with caution because this behavior indicates your debt burden has increased increase, which will negatively impact your score.

How can I improve my CIBIL Score?

You can improve your Credit Score by maintaining a good credit history. This will be viewed favorably by lenders and it can be done with 6 simple rules :

Always pay your dues on time: Late payments are viewed negatively by lenders.

Keep your balances low: Always prudent to not use too much credit, control your utilization.

Maintain a healthy mix of credit:It is better to have a healthy mix of secured (such as home loan, auto loan) and unsecured loans (such as personal loan, credit cards). Too many unsecured loans may be viewed negatively.